Heteroskedasticity and Serial Correlation |

您所在的位置:网站首页 › Durbin-watson stat › Heteroskedasticity and Serial Correlation |

Heteroskedasticity and Serial Correlation

|

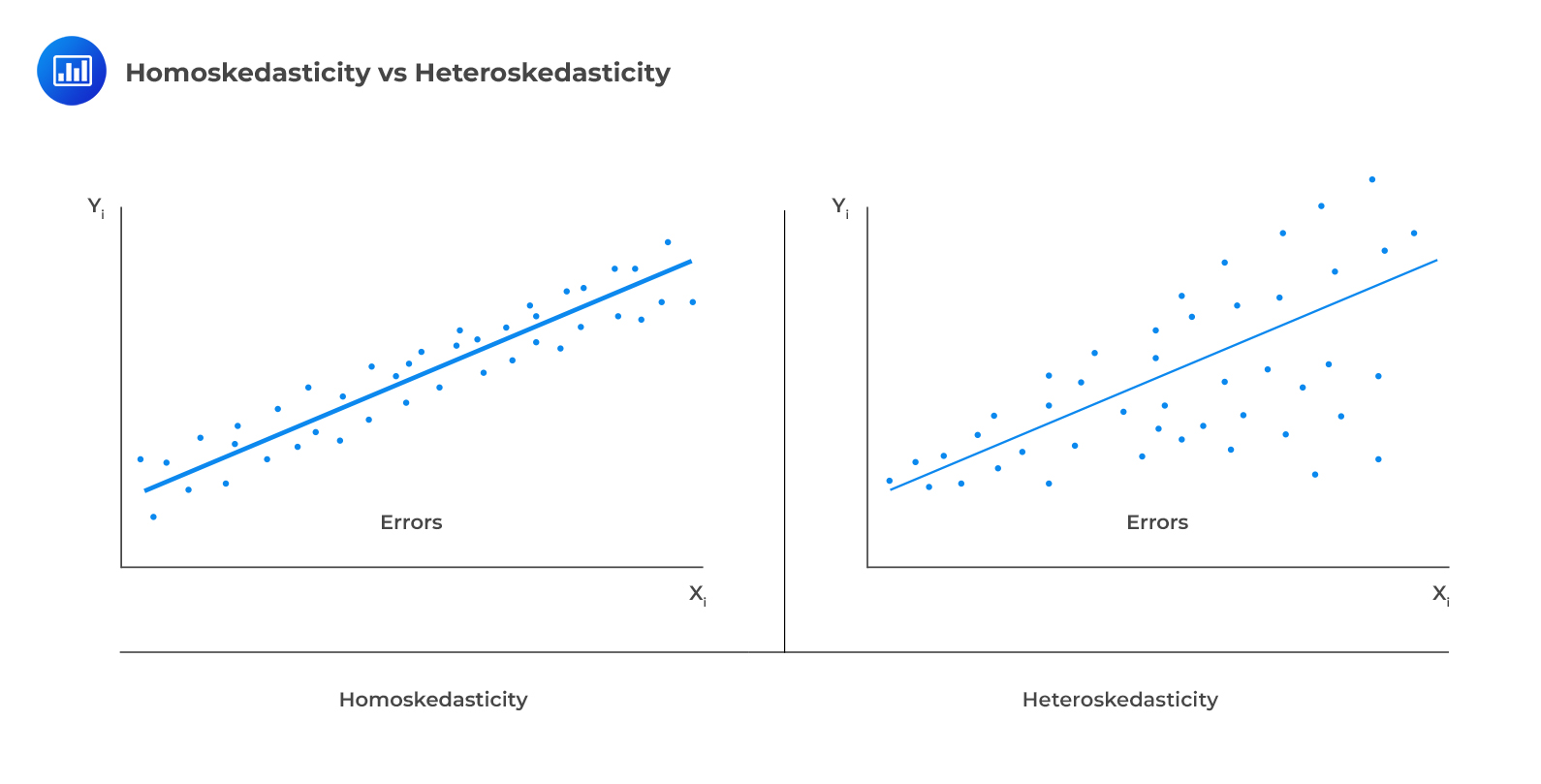

One of the assumptions underpinning multiple regression is that regression errors are homoscedastic. In other words, the variance of the error terms is equal for all observations: $$E(\epsilon_{i}^{2})=\sigma_{\epsilon}^{2}, i=1,2,…,n$$ In reality, the variance of errors differs across observations. This is known as heteroskedasticity. The following figure illustrates homoscedasticity and heteroskedasticity.  Types of Heteroskedasticity

Unconditional Heteroskedasticity Types of Heteroskedasticity

Unconditional Heteroskedasticity

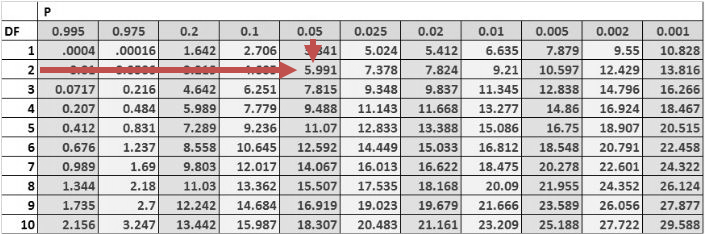

Unconditional heteroskedasticity occurs when the heteroskedasticity is uncorrelated with the values of the independent variables. Although this is a violation of the homoscedasticity assumption, it does not present major problems to statistical inference. Conditional HeteroskedasticityConditional heteroskedasticity occurs when the error variance is related/conditional on the values of the independent variables. It poses significant problems for statistical inference. Fortunately, many statistical software packages can diagnose and correct this error. Effects of Heteroskedasticityi. It does not affect the consistency of the regression parameter estimators. ii. Heteroskedastic errors make the F-test overall significance of the regression unreliable. iii. Heteroskedasticity introduces bias into estimators of the standard error of regression coefficients making the t-tests for the significance of individual regression coefficients unreliable. iv. More specifically, it results in inflated t-statistics and underestimated standard errors. Testing Heteroskedasticity Breusch-Pagan chi-square testThe Breusch-Pagan chi-square test looks at the regression of the squared residuals from the estimated regression equation on the independent variables. The presence of conditional heteroskedasticity in the original regression equation substantially explains the variation in the squared residuals. The test statistic is given by: $$\text{BP chi}-\text{square test statistic}=n\times{R^{2}}$$ Where: \(n\) = number of observations. \(R^{2}\) = the \(R^{2}\) in the regression of the squared residuals.This test statistic is a chi-square random variable with k degrees of freedom. The null hypothesis is that there is no conditional heteroskedasticity, i.e., the squared error term is uncorrelated with the independent variables. The Breusch-pagan test is a one-tailed test as we should be mainly concerned with heteroskedasticity for large values of the test statistic. Example: Breusch-Pagan chi-square testConsider the multiple regression of the price of the USDX on the inflation rates and the real interest rates. The investor regresses the squared residuals from the original regression on the independent variables. The new \(R^{2}\) is 0.1874. Test for the presence of heteroskedasticity at the 5% significance level. Solution The test statistic is: $$\text{BP chi}- \text{square test statistic}=n\times{R^{2}}$$ $$\text{Test statistic}= 10\times0.1874=1.874$$ The one-tailed critical value for a chi-square distribution with two degrees of freedom at the 5% significance level is 5.991.

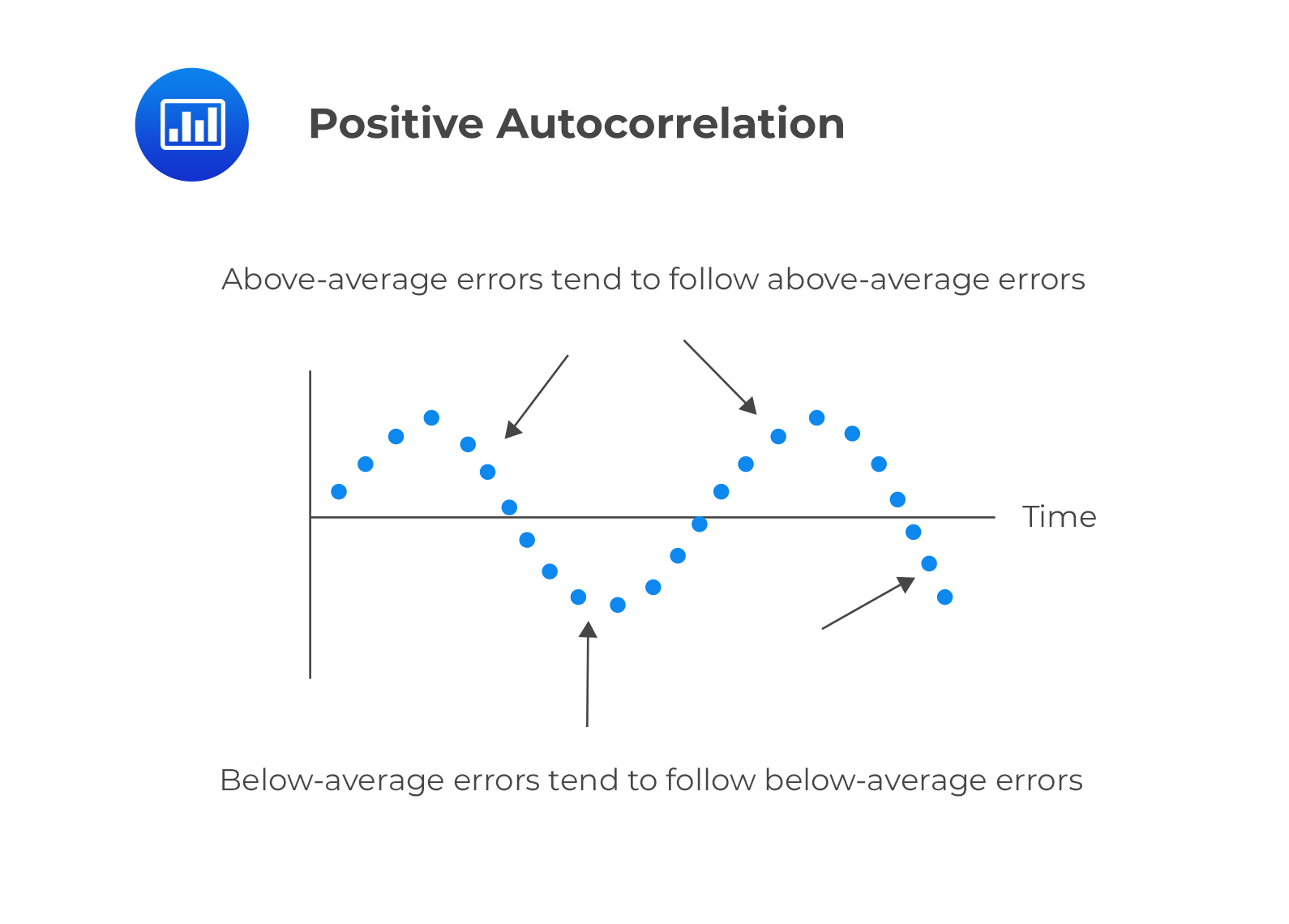

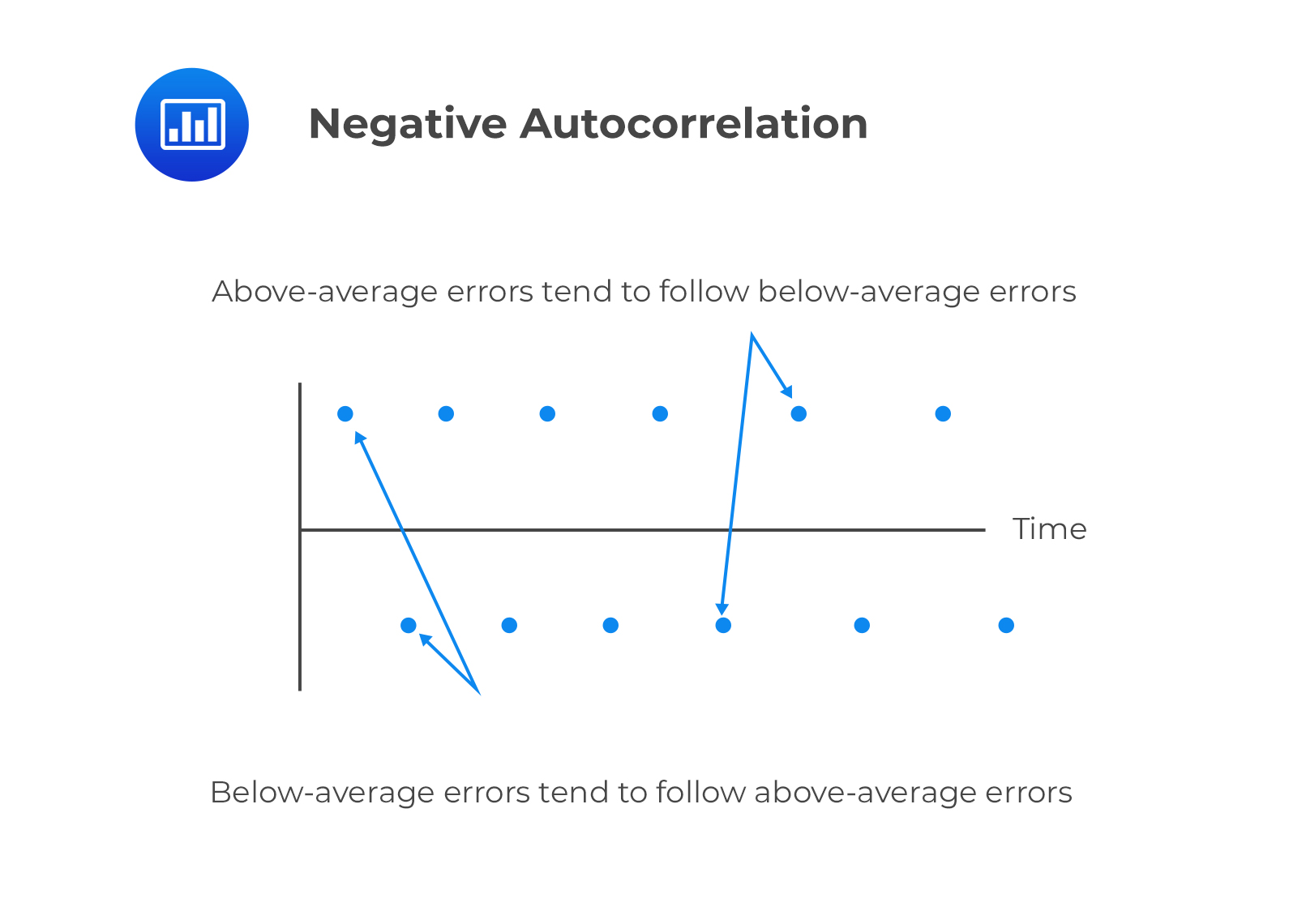

Therefore, we cannot reject the null hypothesis of no conditional heteroskedasticity. As a result, we conclude that the error term is NOT conditionally heteroskedastic. Correcting HeteroskedasticityIn the investment world, it is crucial to correct heteroskedasticity as it may change inferences about a particular hypothesis test, thus impacting an investment decision. There are two methods that can be applied to correct heteroskedasticity: Calculating robust standard errors: This approach corrects the standard errors of the model’s estimated coefficients to account for the conditional heteroskedasticity. These are also known as white-corrected standard errors. These standard errors are then used to calculate the t-statistics again using the original regression coefficients. Generalized least squares: The original regression equation is modified to eliminate heteroskedasticity. The modified equation is then estimated, assuming that heteroskedasticity is no longer a problem. Serial Correlation (Autocorrelation)Autocorrelation occurs when the assumption that regression errors are uncorrelated across all observations is violated. In other words, autocorrelation is evident when errors in one period are correlated with errors in other periods. This is common with time-series data (which we will see in the next reading). Types of Serial Correlation Positive serial correlationThis is a serial correlation in which positive regression errors for one observation increases the possibility of observing a positive regression error for another observation.  Negative serial correlation Negative serial correlation

This is serial correlation in which a positive regression error for one observation increases the likelihood of observing a negative regression error for another observation. Effects of Serial CorrelationAutocorrelation does not cause bias in the coefficient estimates of the regression. However, a positive serial correlation inflates the F-statistic to test for the overall significance of the regression as the mean squared error (MSE) will tend to underestimate the population error variance. This increases Type I errors (the rejection of the null hypothesis when it is actually true). The positive serial correlation makes the ordinary least squares standard errors for the regression coefficients underestimate the true standard errors. Moreover, it leads to small standard errors of the regression coefficient, making the estimated t-statistics seem to be statistically significant relative to their actual significance. On the other hand, negative serial correlation overestimates standard errors and understates the F-statistics. This increases Type II errors (The acceptance of the null hypothesis when it is actually false). Testing for Serial CorrelationThe first step of testing for serial correlation is by plotting the residuals against time. The other most common formal test is the Durbin-Watson test. Durbin-Watson TestThe Durbin Watson tests the null hypothesis of no serial correlation against the alternative hypothesis of positive or negative serial correlation. The Durbin-Watson Statistic (DW) is approximated by: $$DW=2(1-r)$$ Where: \(r\) = Sample correlation between regression residuals from one period and the previous period.The Durbin Watson statistic can take on values ranging from 0 to 4. i.e., \(0 |

【本文地址】